Financial Inclusion – PMJDY – India Post Payments Bank

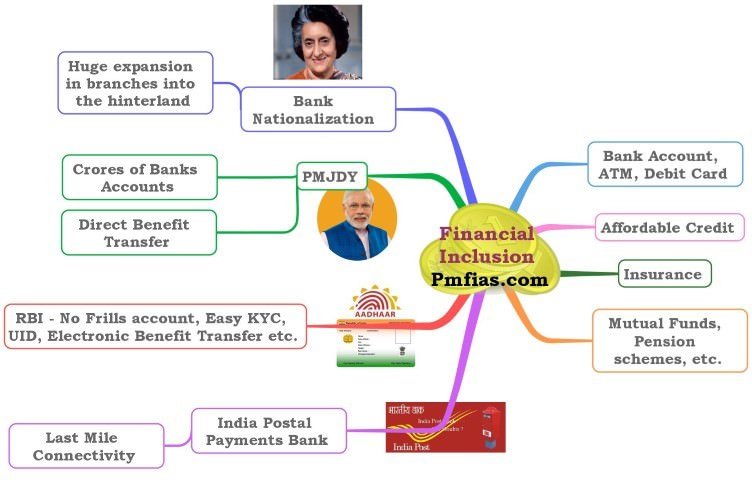

Financial Inclusion

- Financial inclusion means the delivery of basic financial services (banking services) to every section of the society at affordable prices.

- Offering affordable financial services to the disadvantaged and low-income segments of society is the key objective of financial inclusion.

Importance of Spreading Financial Inclusion (FI)

- Majority of the Indian population remain unbanked and their credit needs are served by informal channels which are avenues for exploitation.

- The condition is worse in rural areas and among the weaker sections of the society.

- This has led to financial instability among the lower income groups.

- This dire scenario needs to change and FI offers the immediate solution. It can spearhead the process of fixing most of the economic weakness of India.

Efficiency in public service delivery

- FI will improve efficiency in public service delivery by trickling down (plugging leakages) the public funds such as subsidies, pensions etc. through direct transfers to the intended ones. (Direct Benefit Transfer or Electronic Benefit Transfer)

- Efficiency in public service is the key to narrow down poverty and establish an egalitarian society.

- Financial inclusion also creates awareness towards social security schemes related to pensions, rural employment etc.

Formal channels of credit

- FI has the potential to liberate the poor from the clutches of moneylenders by catering to their ‘affordable credit’ requirements.

Economic progress in Rural areas

- Financial inclusion is key to generating employment in rural areas. Financial inclusion combined with Digital Inclusion has the potential to change the face of rural India.

FI can reduce the menace of Black Money

- Not having a bank account = No ATM, Net Banking = People transact using hard cash = Good market for Fake Currency.

- FI will improve the state of financial literacy and banking awareness in India.

Alternate Investment Options

- Financial inclusion creates awareness regarding Alternate Investment Options like mutual funds, insurance schemes, government securities and other such investment options.

FI could be key to Inflation Targeting

- Alternate Investment Options make inflation targeting easy as banks will have to greatly depend on the money from RBI (RBI can tame the banks).

- Inflation targeting is done by controlling the flow of money in the economy.

- RBI uses Repo rate, reverse repo rate and other monetary policy tools to control the money flow in the economy.

- Due to poor financial inclusion, banks, in the short term, insulate themselves from the impact of RBI’s monetary policy changes. (Less FI = Less avenues of alternate investment = most money saved in bank accounts = bank can use this money to counter the inflation targeting measures of RBI.)

- This makes inflation targeting a hard task for the RBI.

Efforts towards Financial Inclusion

Nationalization of Banks 1969

- Indira Gandhi’s move to nationalize 14 banks in 1969 (with another six being nationalized in 1980) is one major shot at improving FI.

- Initially it faced a lot of criticism.

Positives of Nationalization

- Bank nationalization saw a huge expansion in branches into the hinterland.

- It improved formal credit system and reduced the influence of moneylenders. [Farmers and poor get timely loans these days. Thanks to nationalization of banks.]

- Despite initial setbacks, it benefited both the economy and the PSBs [~2,70,000 people are employed by SBI group].

Negatives

- Investments in branches and the servicing of millions of small accounts pushed up operational costs in nationalized banks.

- Combined with bad loans, the investment resulted in the net worth of public sector banks turning negative by the early 1990s.

Changed scenarios

- At the same time, India’s economic growth began to accelerate in the 1990s (post LPG reforms).

- In these new conditions, the long-run benefits of financial inclusion began to kick in.

PM Jan Dhan Yojana

- Launched by NDA government to further improve financial inclusion.

Comprehensive Financial Inclusion Plan (CFIP)

- The Pradhan Mantri Jan-Dhan Yojana is a part of Comprehensive Financial Inclusion Plan (CFIP).

Aim of CFIP

- CFIP hopes to extend coverage of basic financial services to all excluded households.

Six pillars of PMJDY

- PMJDY consists of 6 pillars.

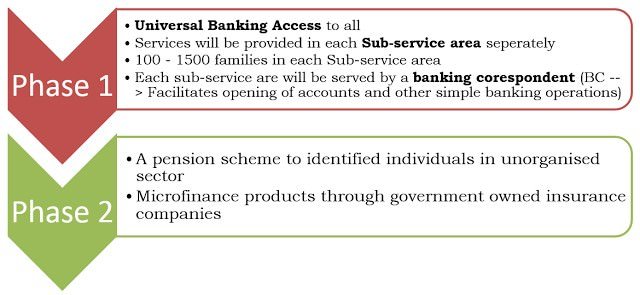

Phase I (15th August, 2014 – 14th August,2015)

- Universal access to banking facilities.

- Financial Literacy Programme.

- Providing Basic Banking Accounts with overdraft facility of Rs.5000 (permits an account holder to withdraw Rs. 5000 more than they have in their account – but this comes with lot of hidden rules – it was just a marketing gimmick) after six months and RuPay Debit card with inbuilt accident insurance cover of Rs 1 lakh and RuPay Kisan card.

Phase II, beginning from 15th August 2015 upto15th August,2018

- Creation of Credit Guarantee Fund for coverage of defaults in overdraft A/Cs.

- Micro Insurance.

- Unorganized sector Pension schemes like Swavlamban.

Other Facilities provided by PMJDY

- After satisfactory conduct of accounts it is proposed to offer reasonable need-based credit facilities.

- A smart card (RuPay card) will be issued to enable customers to operate their accounts even without Banking Correspondents.

Factors that affect PMJDY

Technology adaptation

- Digital India and advanced technology adaptation by banks.

Improving the system of business correspondent

- Banking correspondent is the agent of the banks that serves the rural banking needs where the penetration of formal banking and branches has been negligible. [Last mile conncetivity]

- Can be done by extending BC jobs to kirana shops, and other local unemployed youth.

- BCs need to be properly remunerated and have the full support of banks.

[Unfortunately BC system did not work. Now the government is looking towards India Post Payments Bank]

Easy E-KYCs with the help of Aadhaar

- Insistence on KYC (know your customer) norms has hindered the opening of new accounts. RBI has made efforts to make the process simpler.

- Aadhaar has helped rural populace get an identity so that they can easily meet the KYC requirements.

Improving Mobile banking service

- Mobile banking through phones play an increasingly important role in a scenario where physical bank branches will be few.

Commercial viability

- Past experience suggests that without proper incentives, banks will be saddled with a large number of dormant accounts. [Unnecessary burden]

Criticism of PMJDY

Costly and unviable

- It will create huge stresses in the banking system.

- Many of the new accounts created by inclusion initiatives remain inoperative.

Financial shocks

- The scheme exposes the money of the rural poor to external financial shocks.

[But India has a robust regulatory system that can handle external shocks effectively. India has done well in recent years in spite of deteriorating global economy]

Many loopholes

- Most of the facilities like accident insurance cover, overdraft facility etc. have money loopholes which the common man doesn’t understand.

What proponents say

- It brings in low-cost deposits through savings and current accounts. For PSBs, the high proportion of low-cost deposits turned out to be a source of competitive advantage.

- It could see the household saving rate go up and boost the overall saving rate.

- Improve PSBs which have been losing market share to new private sector banks.

- Financial inclusion entails upfront costs but begins to pay off once a certain scale has been reached. [Bank Nationalization proved this]

- Large amounts are poised to flow into bank accounts, thanks to the direct benefit transfer scheme (DBT).

Steps taken by RBI to support financial inclusion

Initiation of no-frills account

- No-frills accounts cut cost as well as complexity. These accounts focus only on basic facilities by cutting down extra frills that are of no use for the lower sections.

- RBI also eased KYC (Know Your customer) norms for opening of such accounts.

Business correspondents

- The banks have adopted the business correspondent model to facilitate banking services in those areas where banks are unable to open branches.

- Business Correspondent is the agent of the bank that will take financial services to the doorsteps of the rural public.

EBT – Electronic Benefits Transfer

- Human-less transfer of payments and services have reduced costs and the need for government monitoring.

India Post Payments Bank [IPPB]

“India Post Payments Bank could become the most effective vehicle of real financial inclusion in the country.” Critically analyze this statement.

- The India Post Payments Bank (IPPB) is a yet to be started state-owned commercial bank.

- The Union Cabinet in June, 2016 cleared the proposal for postal payments banks with a corpus of Rs.800 crore.

- The new bank is expected to commence operations by March 2017 and will set up 650 branches and 5000 ATMs across the country.

- IPPB can be the real game changer in taking financial services to the doorstep of the rural households.

- The failure of Banking Correspondent system leaves a lot of void which can be filled only by IPPB.

How it works?

- India’s 1.3 lakh postmen will be given hand-held devices, a moving ATM to provide banking services, insurance, money-order, as well as third-party services.

Inherent Advantages of IPPB

- Physical presence across 1.55 lakh post offices with 1.3 lakh postmen touching the farthest corners of the country.

IPPB is a result of Proactive governance

- In 2006, it was announced that India Post would open a bank to erase its ₹1,000 crore deficit emulating Poste italiane.

- In 2014, RBI gave in-principle banking licences to IDFC and Bandhan Financial Services but India Post was not considered because it had not received the mandatory clearance from the (mute) government.

- The rest is history.