Finance Commission (FC): Composition, Role and Issues | 16th Finance Commission

- Context (TH): The GoI appointed the 16th Finance Commission (FC) to determine the vertical distribution of revenue between the Centre and the States and the horizontal devolution between states.

About Finance Commission (FC)

- The Finance Commission (FC) is a constitutional body constituted by the President under Article 280 of the Constitution.

- It is a Quasi-Judicial body constituted every 5th year or at such earlier time as the President deems necessary.

- It consists of a chairman and 4 other members to be appointed by the President. They are eligible for re-appointment.

")

Qualifications of the members of the Finance Commission (FC)

- Qualifications of the members are to be decided by the Parliament, as provided in the Constitution.

- Accordingly, the Parliament has specified the following specifications:

- The Chairman should be a person with experience in public affairs.

- The members should be selected from amongst:

- A Judge of the High Court or one qualified to be appointed as one.

- A person who has specialized knowledge of finance and accounts of the government.

- A person who has wide experience in financial matters and administration.

- A person who has special knowledge of economics.

Recommendations of the Finance Commission (FC)

- The Finance Commission makes recommendations to the President on

- Distribution of net tax proceeds between the Centre and States and allocation between the states of respective shares of such proceeds.

- Principles that govern grants-in-aid to the States by the Centre.

- Measures needed to augment the Consolidated Fund of State to supplement resources of Panchayats and municipalities in the state.

- Any other matter referred to it by the President in the interests of sound finance.

- The Commission submits its report to the President, who lays it before both houses of the Parliament.

- The recommendations made by the Finance Commission are only advisory in nature and not binding on the government.

State Finance Commission

- Constitutional Basis: The SFC was established under the 73rd and 74th Constitutional Amendments in 1992 which aimed to strengthen local self-governance in India by providing constitutional status to panchayati raj institutions and municipalities.

- Appointment: The Governor of each state is responsible for appointing the State Finance Commission every five years, as mandated by Article 243-I of the Constitution.

- Responsibilities: Financial Assessment, Resource Allocation, Grants and Aid, Disaster Management, Policy Recommendations.

16th Finance Commission

- The Government of India has established the 16th Finance Commission under Article 280(1) of the Constitution. Dr. Arvind Panagariya is appointed as Chairman.

Terms of Reference for 16th Finance Commission

- Distributing taxes between the Union and States and allocating State shares.

- Principles governing grants-in-aid from the Consolidated Fund of India to States and grants under Article 275 (empowers Parliament to make law to provide financial assistance to States in the form of grants-in-aid charged to the revenue of India) for specific purposes.

- Measures to boost State Consolidated Funds for supporting Panchayats and Municipalities based on State Finance Commission recommendations.

- Review current financing structures related to disaster management under the Disaster Management Act of 2005, proposing improvements or changes.

Mandate of the 16th FC

- Historical Role: FC has focused on equitable resource redistribution through vertical and horizontal allocations to less-developed states since 1951.

- Tax revenue sharing: Recommend how to distribute tax revenues between the Union government and the states for the five-year period starting April 1, 2026.

- Grants-in-aid: Determine the principles for granting aid from the Consolidated Fund of India to states.

- Urban local govt: Recognise their contribution to economic development & increase allocations to them.

- Beyond Fiscal Arithmetic: The FC’s role is to plan a future where all States contribute to national growth, addressing challenges such as urbanisation and climate resilience.

- Disaster management: Propose improvements to the financing structures for disaster management.

- Climate change: Provide funds for climate mitigation and adaptation measures.

- Fiscal discipline: Advise on fiscal discipline and public expenditure.

- Impact on Growth: The FC’s decisions will influence millions of lives and determine India’s ascent to a leading global economy.

Issues in Financial Devolution

- Firstly, cess and surcharge, estimated at around 23% of its gross tax receipts, are not shared with the States.

- The total tax revenue for the years 2022-23 (actual), 2023-24 (revised estimates) and 2024-25 (Budget estimates) of the Union government is (₹30.5, ₹34.4, and ₹38.8 lakh crore), respectively.

- The State’s share was (₹9.5, ₹11.0, and ₹12.2 lakh crore), respectively, which constitutes around 32% of the total tax receipts of the Centre. This is way less than the 41% recommended by the 15th FC.

- Cess, like the GST compensation cess, is also used for centrally sponsored schemes that benefit the States. However, the States have no control over these components.

- Secondly, the amount each State gets back for every rupee they contribute to Central taxes shows steep variation.

- Industrially developed states received much less than a rupee for every rupee they contributed against states like Uttar Pradesh and Bihar.

- This is because many corporations are headquartered in these state capitals, where they would remit their direct taxes, and there is a difference in GST collection among various states.

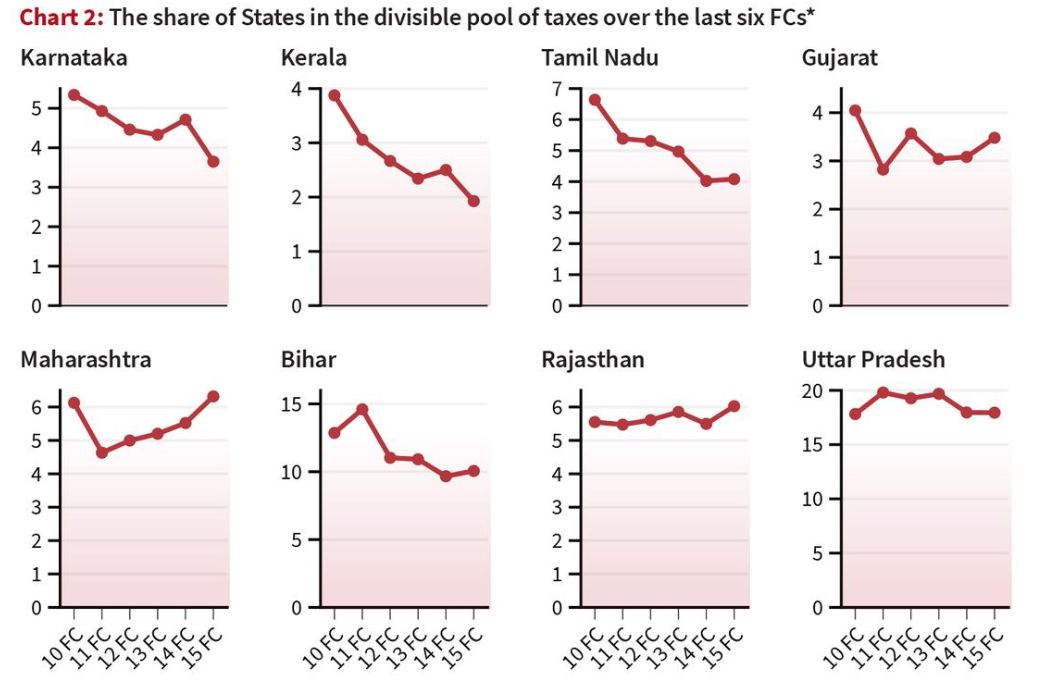

- Thirdly, the percentage share in the divisible pool of taxes has been reducing for southern States over the last six FCs.

- This is due to the higher weightage being given to equity (income gap) and needs (population, area, and forest) than efficiency (demographic performance and tax effort).

- Finally, grants-in-aid varies among various States.

- As per the 15th FC, there are revenue deficits, sector-specific and State-specific grants given to various States, and grants to local bodies. It is based on population and area of States.

Issues with Current Redistribution Policies

- Horizontal Devolution Challenge: Balancing equitable shares for less-developed states with policies that ensure overall national economic growth and fair distribution.

Challenges for Progressive States

- Demographic Changes: Progressive States like Tamil Nadu face declining tax revenues due to an ageing population, necessitating strategies to manage the rising costs and avoid the “middle-income trap.”

- Urbanisation: Tamil Nadu’s rapid urbanisation, expected to reach 57.3% by 2031, requires dedicated funding for infrastructure to sustain growth and meet urban demands.

Need for Progressive Resource Allocation

- Present Shortcomings: Despite the 15th FC recommending 41% vertical devolution, actual devolution dropped to 33.16% due to rising cess and surcharges by the Union.

- Proposed Reforms: Advocate for a 50% devolution of gross central taxes to empower states with greater fiscal autonomy and promote local development.

Way Forward

- Enhanced Resource Allocation: A performance-based resource allocation approach will empower States to drive national growth.

- Urban and Demographic Strategies: Allocating resources for urban infrastructure and demographic adjustments will ensure progressive States like Tamil Nadu remain growth engines.

- Balanced Strategy: A focus on expanding the national economy with equitable distribution ensures benefits for all States, allowing progressive States to continue driving growth.

- Strengthening Policy Frameworks: A balanced distribution policy and targeted support for high-performing States will foster sustained economic development across India.

Vertical Fiscal Imbalance

Importance of Reducing VFI

Role of the Finance Commission in Addressing VFI

Measuring Vertical Fiscal Imbalance

Recommendations for the 16th Finance Commission

|

Related Posts